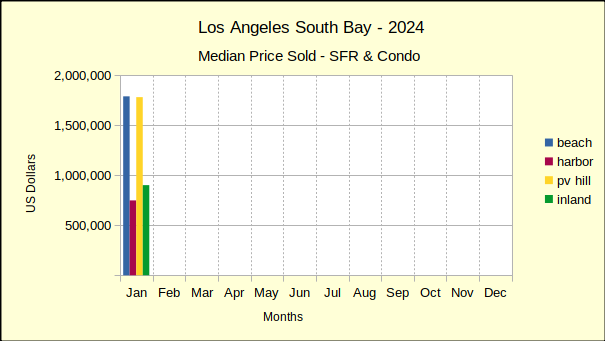

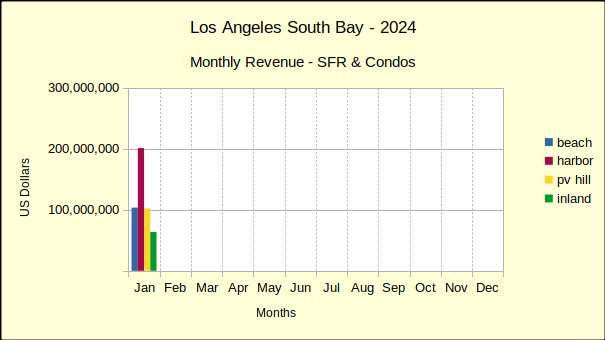

Across the Los Angeles South Bay the number of homes sold in January was down compared to December—way down. For the same time period median prices are mixed with most sales either flat or down.

Looking at sales volume in January versus January of last year, shows big increases in activity. However, that serves more to show how slow the real estate market was at the beginning of 2023, than how good it is today. Median prices were likewise up for most areas when compared to the same month last year.

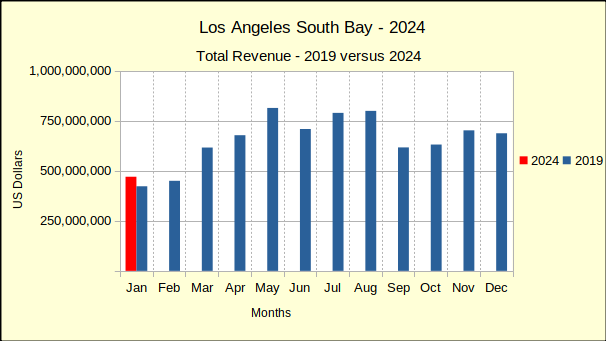

From a historical perspective, looking back at 2019, still the most recent “normal” business year for real estate, we see sales volume overall remains 21% below that benchmark. Median prices, which shot up during the pandemic have stubbornly stayed up. As of January, median prices range from 25-30% above the 2% inflation factor the Federal Reserve targets.

The combination of inflated prices and mortgage interest rates testing the 7% level has created a stagnant market place. Typically a presidential election year would bring rosy news about a growing economy and low interest rates. At this point there’s only one month of data, not enough to make any forecasts, but 2024 is off to a slow start.

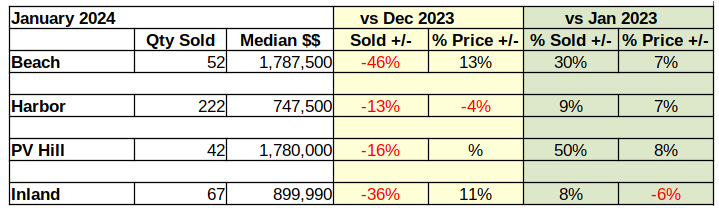

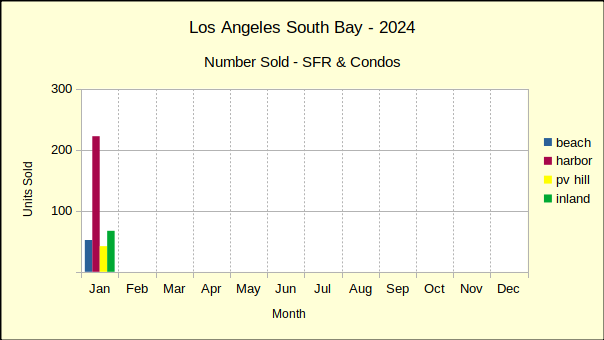

Beach: Sales Off 46%

Month to month sales volume in the Beach cities collapsed by 46% in January. After back to back increases in the number of homes sold for November and December, the huge drop was unexpected. Juxtaposed against the 13% increase in median price, it demonstrates the current market dynamic.

The only actual buyers are people who have no choice but to move, despite the low inventory and high interest rates. At the same time, most sellers are stalling because they don’t want to be sitting on the market for weeks. And, because most sellers are also buyers, they’re waiting for a better market with more homes available and lower interest rates for their replacement purchase. As a result, the number of available homes listed on the MLS is further depressed.

This has brought about a rare phenomenon, the “off-market” sale. Both buyers and sellers are actively looking for deals that can be consummated without the competitive environment of the Multiple Listing Service (MLS). Buyers love the fact there are no bidding wars. Sellers are glad to sell at asking price without endless open houses and dozens of showings. The properties usually end up on the MLS as history, but not as competition. How long this trend will last depends on the economy over the next few months.

The market at the Beach has clearly improved since last year. Sales from January of 2024 have climbed 30% compared to January of 2023. At the same time, median price has moved up 7%. Of course, as mentioned earlier, last January was far from a good market in real estate.

Given the turmoil of recent years, one is compelled to look back at 2019, before the pandemic with it’s rock-bottom interest rates and sky-rocketing prices. Using that metric, January sales this year fell 34% below January of 2019. Median price this January was 43% higher than it was in January of 2019. Clearly “normal” is still a long way off.

Harbor: Sales Off 13%

Month to month statistics from the Harbor area demonstrate a truism. Pointing the way toward stability in the market, many of January’s home sales came with a reduced price. The median price dropped 4%, rather than increasing as it did in the Beach cities. Those price reductions appealed to buyers and the number of transactions increased considerably. Correspondingly, the sales volume only dropped 13% as opposed to a 46% drop at the Beach.

Harbor area sales for January 2024 ended with 9% more transactions than the same month lin 2023 in an unsurprising response to the market collapse of last winter. Also on the positive side, median prices for Harbor area homes increased by 7%.

Pre-pandemic residential sales for January 2024 was mixed in comparison to January of 2019. Sales volume was off, with 16% fewer homes sold in 2024. At the same time, median prices were up 44%.

Hill: Sales Off 16%

November and December of last year looked like a bad thing was turning good, and then January 2024 came along. Home sales on the Hill suffered less than at the Beach or Inland, but a 16% drop in sales volume in an already moribund market hurt. Median prices on the Hill hit that “sweet spot” with no change up or down.

Compared to January of 2023 the number of home sales on the Hill went stratospheric climbing 50% for the month. Of course, having read this far you know last winter was a low spot in the market. Combine that with the comparatively small number of sales on the Palos Verdes Peninsula and it’s easy to have outsize percentages. While sales volume was up 50%, median prices climbed a more modest 8%.

January 2024 versus January 2019 in home sales on the Hill showed an solid improvement. The number of homes sold increased by 27%, in contrast to falling sales in the Harbor and Beach areas. With the number of home sales up, a 37% increase in the median price is a welcome addition.

Inland: Sales Off 36%

Home sales in the Inland area closely followed those at the Beach in January. Similarly, the month ended with a calamitous 36% drop in the number of homes sold—down to 67 homes from over 100 in both November and December. Likewise, the median price came in with an 11% increase, slightly less than at the Beach. This shows the effect of “sticky prices” where a lot of sales don’t happen because the sellers are resistant to lower offers and buyers are balking at higher prices.

On a year over year basis, January 2024 showed 8% growth in the number of sales compared to last January. Median prices continued following the long downward slide of 2023 and dropped another 6%.

Comparing the Inland sales to 2019, the most recent stable year, the number of homes sold has dropped by 39% leaving a lot of room for recovery. The median price has climbed 40% over that five years, roughly 27% greater than the “ideal inflation” sought by the Federal Reserve.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo

Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City

PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates

Inland=Torrance, Lomita, Gardena