Currently, Millennials are the largest group of homebuyers. The second largest is Gen X, who have a fair number of similarities with Millennials despite being in the workforce much longer. Gen X, like Millennials in 2007, also experienced a major recession in 1980 — and a fair number even lost their homes in 2007 that they had only recently been able to purchase. All in all, Gen X hasn’t had much luck with homebuying. They haven’t lost hope, though — the current hot market appears to be attractive to Gen X prospective homebuyers.

The effect is clearer in some cities than others. The most popular metros for Gen X to move to are in the southeast. This includes several metros in Florida, as well as Memphis, Atlanta, New Orleans, Raleigh, D.C., and Baltimore. By contrast, the least popular metros are primarily not in this region, with the exception of Nashville. The others are San Jose, Seattle, Pittsburgh, Austin, Buffalo, Boston, Minneapolis, Denver, and Salt Lake City.

When discussing economic sectors, nonprofits are often lumped in with for-profit businesses, or simply ignored. But ignoring them doesn’t paint a full picture, and they aren’t impacted by economic crises in the same way as businesses. In fact, depending on the type of nonprofit, they aren’t affected the same way among each other, either. One may expect nonprofits to struggle more than businesses that are able to utilize profits as an emergency fund. During this pandemic, that was true for arts and culture based nonprofits, but the opposite was true of basic needs nonprofits.

During an economic and health crisis, food services, support programs, and health education programs are in high demand. Nonprofits focused on these types of projects flourished. Food Finders, which partners with nonprofits to provide food to those in need, acquired 400 new volunteers in 2020 and supplied 6 million more pounds of food than the prior year. Charitable donations in the US are way up, with an estimated 4.1% increase.

The arts, on the other hand, took an enormous nosedive. International City Theatre had a great year in 2019, but 2020 was shocking. Revenue went down a whopping 90% in 2020. The majority of their revenue is one-time subscriptions and ticket sales. No one is going to purchase a subscription while under lockdown, and even though they tried implementing virtual programs, they weren’t in high demand. Fortunately, smaller arts nonprofits weren’t hit as hard, since they have lower overhead costs.

Though it’s been six years since same-sex marriages were legalized in the US, that didn’t mean an end to discrimination. It was only this year that LGBTQ+ discrimination was banned at a federal level. The LGBTQ+ homeownership rate is only 49%, compared to the overall number of 65%. The rate is particularly low for transgender individuals, at a mere 25%.

Part of the lower homeownership rate for the LGBTQ+ community can be attributed to secondary factors, but not all of it. Many of these people live in urban areas, where they are more likely to rent as opposed to buy. But even that has discrimination as an underlying factor, since a major reason they tend to live in urban areas is that these areas are usually more welcoming to the LGBTQ+ community. Moreover, the estimated purchasing power of the community as a whole is $1 trillion. It’s certainly the case that more than 49% of them have the income to purchase a home.

The fact is that LGBTQ+ people face discrimination not only from their communities, but also from real estate professionals and lenders. Less than a quarter report no discrimination at all. 13.8% say they signed documents that misrepresented themselves in order to get their documents in order. 10.6% report discrimination from real estate professionals and 5.2% from sellers. It’s not just prospective homeowners, either; 5.3% of LGBTQ+ members attempting to rent a home were denied by the landlord. Fortunately, with the anti-discrimination order being signed this year, things are looking up.

Prior to the increasing popularity of work from home models, most people only travelled on vacation when, well, on vacation. While they were working, they needed to live close enough to work to have a reasonable commute. That meant resort areas such as Palm Springs and Lake Tahoe didn’t have a high permanent population, just a lot of transient residents, especially during holidays. Now, these areas are in high demand for homebuyers who wish to live there permanently.

It’s true that vacation towns are generally expensive. You’ll get that anywhere where tourism is a major source of the city’s income. But the 30% price jump in Palm Springs over the past year was not because of tourism, since tourists don’t buy houses there. Demand is increasing for areas close to recreation, since the same people can also work there, at their new home, instead of commuting. This is especially true of outdoor recreation, but even Truckee, with its numerous art galleries and clothing boutiques, doubled its median home price.

Some of these towns are struggling to take in new residents, though. Housing can’t be built overnight. While vacation towns often have more than enough space for their relatively small number of permanent residents, it’s frequently in the form of hotels, AirBnBs, and second homes. The former two are generally still occupied as well, just not by their owners.

If you have a large family, or are expecting your family to grow, chances are you’re thinking you need a lot of space. That’s not necessarily the case. A little can go a long way if you have the right kind of space. Here’s what you should be looking for.

Your primary focus should not be living space, but rather storage space. A person doesn’t take up a lot of room. But for each person in your family, there’s going to be some space that needs to be dedicated to their belongings. This means you’ll need closet space and cabinets, or maybe an attic, not expansive bedrooms or large living rooms. The total size of your house isn’t as important as what functions it can serve.

Speaking of functions, the right functions for your family may be different than those of another family. Some families like to all sit down together for dinner, and want a dining room that can accommodate a large dinner table. Other families would benefit more from a game room for Friday game nights. Also keep in mind that if a space is flexible enough, it could serve the purpose you want even if it wasn’t designed that way. However, it’s important to note the space’s floor plan. Maybe the office is too far away from the bathrooms to benefit from converting it into a bedroom. Perhaps that space that’s the right size for your living room is next to the kitchen and may be better suited as a dining room. Also ask yourself where you want your kids’ rooms to be in relation to each other and yours.

In response to the Covid-19 pandemic, Catalina Island was closed to tourism. Tourism is a major economic sector on the island, making the pandemic a significant economic crisis in addition to a health crisis. With Catalina Island now reopened, tourists are eager to get in on the fun. Tourist activities include kayaking, zip lining, outdoor recreation classes, hiking, tours, fishing, and souvenir shops.

On May 13th, the CDC dropped the recommendation of wearing a mask for fully vaccinated persons. However, the CDC guidelines are only recommendations, not law. Federal, state, and local laws still apply. California law still has a mask requirement, so even fully vaccinated people should still be wearing masks inside businesses. The state has opted to wait until June 15th to remove this requirement.

Not everyone in California is vaccinated yet, particularly in underserved communities. The hope is that the four week period will help ensure more people are vaccinated, as well as give businesses time to readjust to the new regulations. Vaccination progress will be monitored. Current trends are good, so if they continue as they have been, vaccinated people should be able to keep their masks off after June 15th. Of course, the virus doesn’t care about laws — it may still be there after that date, so if you want to stay safe, nothing is preventing you from continuing to wear your mask until you feel comfortable.

In Long Beach, construction has now started on a seven story residential building on The Promenade. The structure, currently named The Inkwell but subject to change, will have 189 units as well as 10,000 square feet of commercial space on the ground level. It will also have a fitness room, club room, pool decks, and pool. Subterranean parking is available, with 268 car stalls and 40 bike stalls.

The Promenade is an established commercial district, with multiple popular restaurants within walking distance of the new building. Business owners in the area have mixed feelings about the new construction. While it’s sure to bring more traffic to the area once it’s completed, we can guess that’s probably 18 to 24 months away from now. In the meantime, dust and construction noise are likely to cause a dropoff in activity for local businesses, particularly during lunch hours. Some of these businesses are just getting back on their feet after a rough time during the pandemic.

2020 saw a large increase in mortgage originations, particularly refinances, as a result of low interest rates. It was expected that this would start to fall off in 2021, since interest rates are starting to go back up. However, they’re still low enough that refinances continue to be common. The statistics are a bit misleading for purchases, though. Low inventory is boosting home prices, accounting for a significant part of the increase in loan origination dollar amount even beyond increasing the number of loans originated.

Something is still missing, though. Even though much fewer loans are delinquent now than in 2020, the share of them that are over 90 days delinquent is increasing. This is because people continue to tread water through moratoriums, but aren’t earning any money. Jobs still haven’t recovered from 2020. Foreclosure moratoriums and forbearance programs are going to end eventually, and that’s going to be a problem for some people who have lost their jobs during the pandemic and haven’t been able to find work yet. If home prices continue to rise without an actual jobs solution, these stopgap measures are going to be the proverbial dam that causes the market to crash when it breaks.

California is the most populous US state, and as with every state in the nation, the population is continually increasing. Well, most of the time. California’s population actually decreased from 2018 to 2019 for the very first time, albeit only by 0.1%. From 2010 to 2020, California’s population growth of 6.1% was 1.3% below the national average of 7.4%. Growth has been on a decline for quite some time: It was 13.8% in the 1990s and 10.0% in the 2000s. In fact, California is set to lose one of its congressional seats due to lack of population growth.

There are several factors that combine to account for this. Birth rate has declined in recent years, with younger generations waiting longer to have children, or not having children at all. The death rate also increased by 26% between 2019 and 2020. California’s immigration rate is also slowing, partially due to increased housing costs. Increased housing costs primarily affect the more expensive coastal cities, which are the areas that saw actual population decreases in 2019; less expensive areas of California had increases in population. Rising prices can be traced back to slowing construction, which in turn is partly a result of strict zoning laws, and has been exacerbated by job losses due to the pandemic and recession.

Appraisers may have to make some minor personal judgments when examining a property’s potential value, but they have less leeway than you may think. There are several factors that an appraiser must take into consideration. It’s important to realize that an appraiser’s job is to report a property’s value, not determine it. The factors that an appraiser looks for include those related to the property itself in addition to the surrounding environment.

The property’s individual characteristics are called elements of value, and they can be remembered using the acronym DUST. They are demand, utility, scarcity, and transferability. Demand is the same for an appraiser as it is for anyone else — the number of buyers who may be interested in the property. Utility looks at all of the property’s potential uses. Scarcity is similar to supply, but is specific to properties similar to the one in question. Transferability relates more to the seller than the property itself, and simply asks whether the seller is legally able to transfer the property.

The environmental factors include physical, economic, government, and social considerations, or PEGS. Physical considerations are the property’s proximity to various resources, such as public transportation or amenities, and even natural resources. Economic factors include data such as rents, vacancies, and homeownership rates, as well as employment opportunities. Among the government considerations are property taxes, zoning and building codes, and local government services. The social aspects are such things as crime rates, school ratings, and recreation.

We’ve mentioned several times already how cutthroat the competition is in the current housing market, and how this is raising already high prices. The effect on people across the industry — such as buyers, sellers, lenders and real estate agents — is apparent. One group that you wouldn’t think would be strongly affected is appraisers, since their pay isn’t affected by home prices. In reality, they are beginning to struggle. Not only do they have much higher demand when the market is hot, but it actually makes their job much more difficult.

Appraisers are often using values of recently sold homes as a point of comparison. While this is not the only tool appraisers have at their disposal, it’s a major one, and its efficacy is called into question in the current market. Houses are selling very quickly, and prices are rising rapidly. Adjusting the formulas to account for a sudden burst of competition isn’t easy. In addition, an appraiser’s job isn’t to predict the future. Even if we can see that the market is unstable, or heading in a particular direction quickly, an appraiser reports the current value of a property, not what its value may or may not be in the near future. These factors all result in undervaluation of properties, which we can see sellers or their agents are also doing as many properties are selling well over the asking price.

Buying a home can be a stressful process, especially if it’s your first time. But there are several things you should consider beforehand to make sure you know what you’re getting into. If you come up with a solid plan, you won’t be as nervous when it comes time to make an offer.

The first thing you should do is check your credit score. If your credit score is below 620, private loans may be more difficult to acquire or come with high interest rates. Having poor credit may not be a good thing, but at least by knowing your credit score, you know you’ll be looking at a government-backed loan. If your credit score is good, you’ll have more options.

Examine your long-term budget closely. Keep records of income and expenses, and gather together your financial documents, such as pay stubs and tax returns. Not only will this help you personally understand your budget, some of these documents are used by lenders for prequalification or preapproval. Prequalifications estimate your ability to pay to give a solid idea of what range of prices you can probably afford. Preapproval is the next step, after you’re more sure of an area and timeframe in which you want to buy. Once you know what your options are, you need to research all of them. If you can, go to multiple lenders and shop around for the best interest rates. Be sure to ask questions.

Even if you get a preapproval, that doesn’t mean you can immediately breathe a sigh of relief. Preapproval is based on your current levels of income and expenditure. Lenders will be consistently re-checking these until the loan closes. If you make any sudden financial moves, they will know, and your credit score will suffer. Not to mention you may not actually be able to afford the house you plan to buy if you suddenly lose your income due to quitting your job, or drop a bunch of money on new furniture. If you are considering something major, call your lender and discuss it with them, before you decide to do it.

If you’re looking to buy a house, unless you intend to pay cash, you’re going to need to get a loan. One obstacle to getting a loan is having a low credit score — if lenders don’t trust that you’ll be able to pay them back, they won’t want to give you a loan. Even if they are willing to lend you money, they will do so at a higher interest rate. Your credit score ranges from 300 to 850, with 800 or above being considered excellent credit, though most people have a credit score between 600 and 750. If you want to know your credit score, or check for errors or fraud, you are entitled to one free annual credit report on AnnualCreditReport.com from each of Equifax, Experian, and TransUnion.

The easiest way to ensure that your credit score doesn’t drop is to make bill payments on time. You may think that as long as the payment gets made, it doesn’t matter if it took a bit longer to get the money to them. That’s not the case, as payments made 30 days late or more can stay on your credit report for up to 7 years. If you are allowed a minimum payment, such as on credit card bills, even making the minimum payment on time is better than waiting until you have the full amount. If you do find yourself in debt, paying down existing debt will also increase your credit score. One thing that you may not realize affects your credit score is the timing of applying for cards. If you apply for several credit cards in a short time period, it looks like you’re wanting a large amount of cash very soon, and may not have the money to pay back loans.

The National Association of Realtors (NAR) has been pushing for an end to the eviction moratoriums, citing the struggles of landlords who are losing profits without either getting payments or having any occupancies to fill. This isn’t an unexpected position, since 38% of NAR members are landlords, but it’s clearly in their personal interest and not the interest of the majority. Beyond this, only 1.8% of landlords are actually delinquent in their mortgage payments, so the majority of them aren’t truly struggling too much. Furthermore, there’s actually a better solution even for the small percentage of landlords that are having issues.

Ending the eviction moratorium is not going to do anything to enable people to afford rent payments. It could help landlords slightly by reducing their upkeep costs, but it’s not likely to bring in new renters. Most units would remain vacant, merely exacerbating the homelessness issue in the US and weakening efforts to curb the ongoing pandemic. California’s SB 91 is a good example of a better solution: It keeps tenant protections in place while still giving landlords 80% of the rent payments they would receive, in exchange for waiving 20% of the payment. This is a better deal for the landlords than evicting their tenants if the unit is simply going to remain vacant. More efforts like this one are going to be the solution to this crisis, not ending eviction moratoriums.

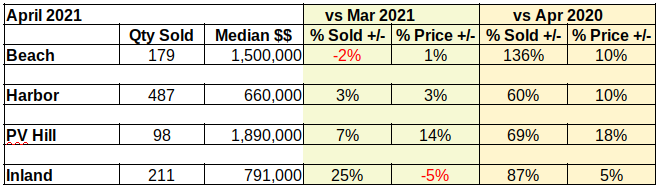

As we discussed in this column last month, comparative analysis of real estate between “the year of Covid” and any other year will be relatively meaningless. Starting in August we may have something approaching useful data in the year-over-year category. Until then, the best guidance will come from the month-to-month numbers and paying close attention to buyers and sellers.

The Beach cities is a great example. A 2020-to-2021 comparison of March sales shows an increase of 136%. Compare that to the March-to-April decrease of 2% and we immediately see the dramatic difference. The table below shows how huge the difference is. The year-0ver-year statistics are all skewed way to the high side because there were significantly fewer sales in 2020 than in a normal year.

Moving on to the monthly statistics, let’s look at how the year is shaping up. There was a minor decrease of-2% in the quantity sold at the Beach last month. The rest of the South Bay showed increased sales, with the inland cities showing a big bump up, in addition to a lower median sales price.

Entry level buyers who can now afford to become home owners, due to pandemic stimulus interest rates, make up a big part of those added sales. Another sizable component is made up of investors who can make cash offers, then leverage their investment to do it again.

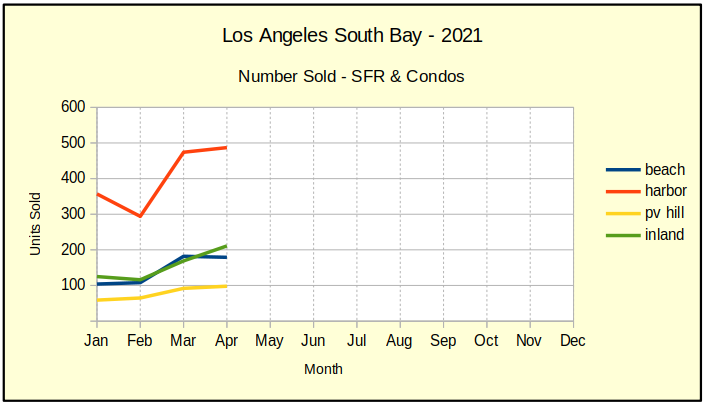

Slowdown in Volume of Sales

The chart below shows steep growth in the number of homes sold in all areas for March. Sales in the Harbor cities were especially strong. It looked like the bright light at the end of the Covid tunnel. But, in April we see sales level off everywhere except the inland cities. The pent up demand we spoke of last month seems to be easing already.

When the volume of sales drops off, there is typically a decline in the price point, too. So far prices have been on the ascendant. The low interest rates kept buyers in the market, and the shortage of homes drove the prices up.

Home buyers are typically most active in the months surrounding school vacation for students. No parent wants to change schools during a regular session. We’re in the month of May, and the sales stats coming out next month will give us a better picture of how much recovery we will see this summer.

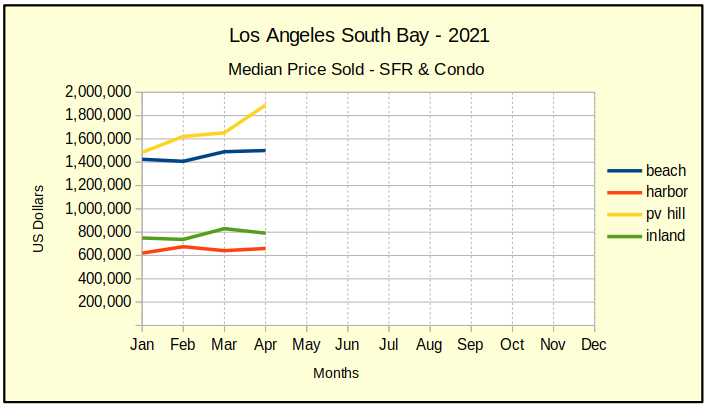

Prices Level Out Across South Bay

Like the number of sales, the median prices have flattened and in some cases turned down this month. Palos Verdes homes seem to have taken a strong upward trend with a 14% jump in price. However, looking a little deeper we find there were two exceptionally large sales which combined to create an illusion in the charts. That yellow line should drop back down around $1.6M next month.

Considering the rate at which prices have been increasing over the 2020 prices, leveling off is a necessary thing. In each of the first four months of this year, home prices have escalated as much as they would in a normal year. Continuing at this rate threatens us with another “bubble” coming on the tail of Covid-19.

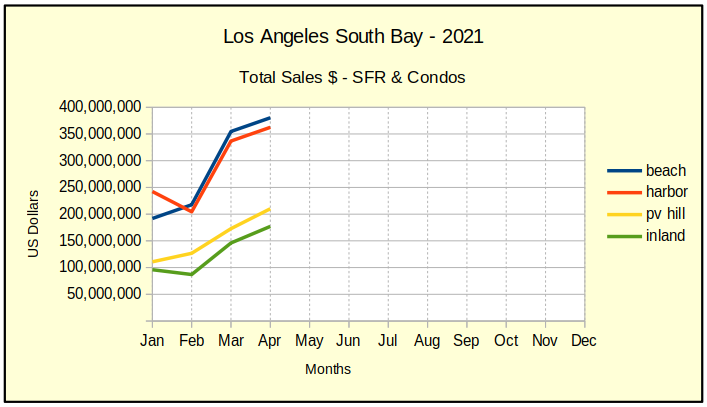

Total Sales Dollars Still Climbing

Elevated prices combined with increased sales last month to push total monthly sales dollars way up. The chart looks like everything is hunky-dory. If only we didn’t know this is growing out of the disaster we lived through in 2020.

Actually, we’ll be quite lucky if some excessive price increases are the only fallout from the pandemic. We’ve written a number of articles recently on the probability for a rash of foreclosures coming after June 30, when the prohibition of eviction and foreclosure come to an end. Stay tuned and we’ll keep you abreast of the situation as it develops.

Contrary to popular belief, there is no governmental license designated as a “property management” license. The Institute of Real Estate Management (IREM) does have a Certified Property Manager (CPM) designation; however, the IREM is a private company and not a regulatory organization. There are also other third party certifications. It may be useful to have these certifications, because it could increase your credibility, but it’s not a legal requirement. That said, there is a government license that is required for some activities of a property manager: a real estate broker’s license.

Not all of a property manager’s activities require a broker’s license, and not all activities requiring a license are performed by all property managers, even if they are licensed. Two common property management services that do require a license are managing the operations of income property and collecting rent. Other things requiring a license are less commonly done by property managers: listing and marketing the property for lease or rent, locating income property, listing prospective tenants, and trading in leasehold interests. A property manager with a broker’s license could also designate an employee to perform these tasks, but the employee must have a brokers-associate license or a sales agent license.

There are still some things you can do as an unlicensed property manager, if you are managing an apartment or vacation rental. You can show available units and facilities, provide information about listed rates and provisions, provide application forms and answer questions about them, and accept screening fees, signed agreements, and rent and security deposits. Note that while a license is required to collect rent for an income property, it is not required to collect rent on apartments or vacation rentals. In addition, no license is required to act as a property manager if the income property owner has given you “attorney in fact” under a power of attorney as a result of temporary inability.

President Biden is due to release his 2022 budget plan in the fall of this year. Though nothing is set in stone yet, we have some ideas about proposed changes Biden plans to make to federal income taxes as well as estate and gift taxes. If any of these come true, it’s likely that the effective date will be January 1st, 2022, though it could be earlier. Here are some of the key proposals that may significantly shake up tax laws.

There are proposed increases to individual income tax rates, capital gains rates, and corporate income tax rates. Under these changes, the maximum individual income tax rate and maximum capital gains rate would likely become equal, both at 39.6%. A major change expected is the repeal of 1031 exchanges, which allow property owners to defer, sometimes perpetually, taxes on property sales when the proceeds are reinvested into real estate. There will probably also be changes to state and local income tax deductions. In the realm of estate and gift taxes, Biden is expected to drastically reduce the exemption amount and increase the tax rate.

Many people may say that a particular property is owned by a trust, or in the name of a trust. Such statements may be pragmatically useful for conveying the idea, but it can lead to confusions. Not everyone is aware that trusts can’t actually own property. Instead, property is in the name of a trustee of a trust, and is held in trust, not by a trust. In addition, trusts for which the grantor is sole trustee are not separate taxable entities. When a property held in trust being titled, the titling should include the name of the trustee plus “trustee” or “as trustee,” as well as the name and date of the trust.

When establishing a trust, your Declaration of Trust is called a trust instrument. The name of your trust instrument must provide the name of the trust in addition to the instrument. Information about the property should be provided in the form of a separate Property Schedule attached to the trust instrument. When providing copies of your trust instrument, such as to banks, many will have their own certification of trust forms for you to fill out instead of copying the entire document. If they don’t, your state may be able to provide such a form. If you can’t find such a form, the relevant pages banks need is generally a page with the grantor’s name, a page appointing the trustee, a page listing the trustee’s powers, and signature pages.

If you’re wanting to sell but don’t think you can get as much as you want for your property, you may want to reconsider. The current market climate heavily favors sellers, as demand is quite high and inventory is low. Cutthroat competition means many prospective buyers are willing to pay significantly more to secure a purchase amid the limited supply.

This is especially true in 11 states, where half or more of sales are for over the asking price. In California and Colorado, a full 60% of properties sell for over the asking price. Only one state, Louisiana, had a percentage of sales over asking below 20%, at 19%. Unfortunately, there is no data available for Idaho, Alaska, or Hawaii.

Though buyers are at a disadvantage in today’s market, you can still use this knowledge to your advantage if you are looking to buy. Expect to pay more than the price range you’re looking for, which means get pre-approval for a higher amount. Be aggressive in your offers, and round numbers up, not down. While there’s always a chance sellers will accept low offers after some time on the market, properties aren’t staying on the market. If you’re not able to afford a solid offer, move on and look elsewhere.