There’s a strong tendency to want to pay off your mortgage as quickly as possible. There’s also a strong reason for lenders to not want you to do that — they get less money because you aren’t paying as much in interest. Because of this, they frequently use prepayment penalties. This is an extra fee for paying off your mortgage too quickly or before the term of the loan ends. If you’re simply paying the minimum amount anyway, this won’t affect you, but if you think you may want to pay off your loan early, you’ll want to know your options.

Different states have different laws regarding prepayment penalties, and some don’t allow them at all. In states where they are allowed, they come in two types: hard prepayment penalties, which are fixed fees regardless of the reason for prepayment and that are usually a percentage of the loan amount, and soft prepayment penalties, which are only charged if the borrower pays a large amount in a short time period. Even in states that allow prepayment penalties, not all loans will have them, and you may be able to negotiate with your lender for their removal. When shopping for loans, make sure to read all the terms of the agreement, and talk to a legal professional if there’s anything you don’t understand or want to learn how to negotiate.

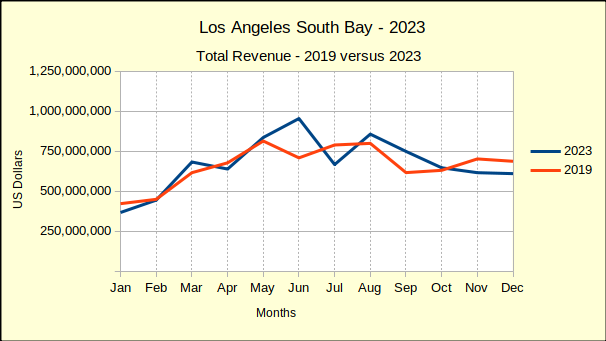

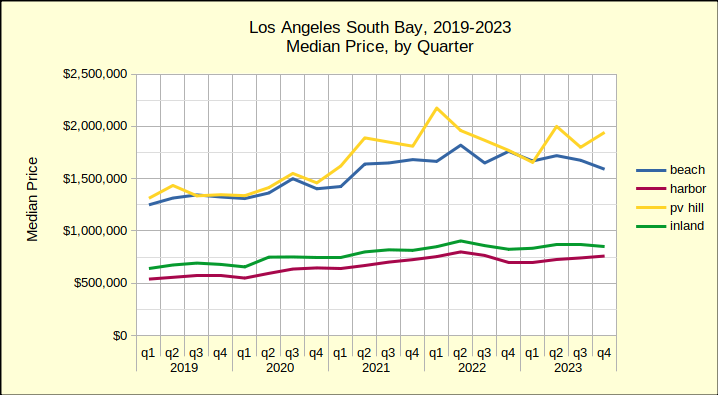

By every measure South Bay real estate failed last year. The volume was down from the prior year in every residential area, the median price fell from 2022 heights everywhere, and the double whammy of crashing sales and falling prices brought the total revenue down from 2022. Judging from early reports the same is true across most of the state.

Part of the story doesn’t read so poorly though. As we look back across the year, the second of half of 2023 was far better than the first half of the year. This in two respects: first, the month-over-month statistics for sales volume have improved. The median price is still falling, but that’s to be expected if we’re going to see a sales volume increase concurrent with continued high interest rates. The market is going to demand that some of the “overly enthusiastic” price increases come back down.

Second, the year-over-year decline in median price is slowing—not reversing—slowing. Roughly speaking, the number of homes sold for less than 2022 prices improved from 83% in the first half of the year to 45% in the second half of 2023. That signifies an approaching balance in the market. Buyers are still holding back, but some sellers are coming forth to meet them.

2024 South Bay Real Estate: Better Days Ahead

We expect to see continued slippage in the median price, accompanied by increased sales volume. The Los Angeles South Bay is somewhat insulated from the vagaries of national and international events, but 2024 is facing an active political climate. The continuing wars around the planet would be enough to rattle economic markets here. This year sellers and buyers also have to factor in a contentious national election.

While the Federal Reserve System is officially apolitical, history has shown a tendency for improved economic conditions during election years. The final quarter of 2023 saw a softening of the wild swings in home sales volume and pricing. With less than 10 months until the presidential elections we anticipate continued easing of interest rates and increased sales activity. Median prices have fallen by about 2% across the South Bay in 2023 and probably won’t drop a lot more in 2024.

Sales volume fell by 15% across the South Bay in 2023. Nearly all of that drop was in the first half of the year. The new year is expected to be positive with growth in sales across the board.

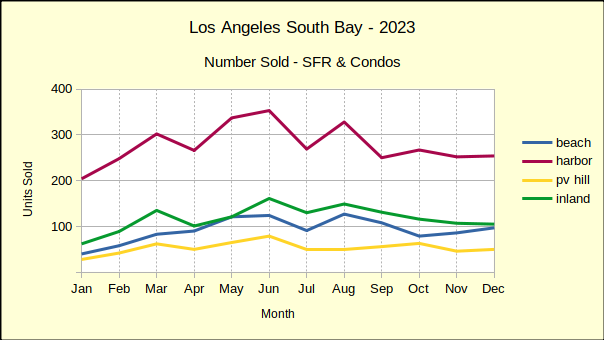

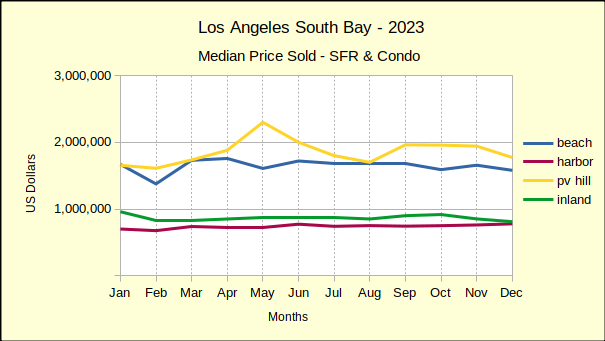

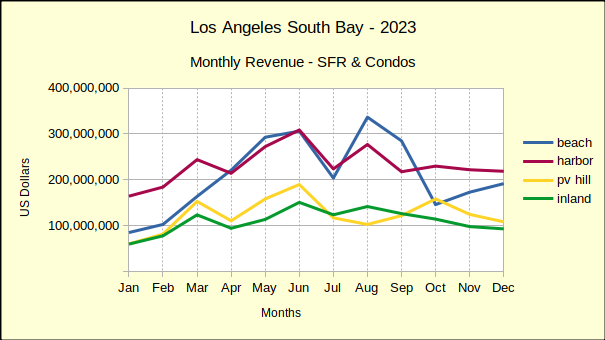

Beach: Strong Sales On Weak Prices

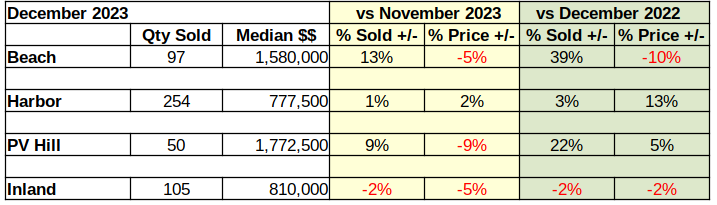

Comparing December to November, the number of homes sold at the Beach was up 13%. That increase in sales is on top of a 9% increase in November, a dramatic turnaround from the 27% drop in October. On the other hand, the month to month median price fell 5% in December.

December of 2023 was similarly mixed when compared to December of 2022. Year over year saw sales volume increase a staggering 39%. Looking back shows December of last year as the absolute slowest month of the year for home sales at the Beach. The median price plummeting by 10% certainly helped generate those December 2023 sales.

Year to date numbers, comparing all 12 months, showed the number of home sales off by 11%. At the same time the median price was down 4% for the year. Much of the annual decline in sales volume occurred in the first half of 2023, when monthly drops of 25%-35% put the brakes on prices. Beach area median prices have taken steep falls since February 2023. It may take a couple more months before the first stimulating news on the interest rate front, but it would appear we’re looking at the “bottom of the market” now. Regardless of whether you’re a buyer or a seller, this is time to reassess your options.

Harbor: Positive Across the Board

December versus November of 2023 saw sales volume go up 1%. During that time the median price went up 2%. Harbor area homes sales dropped precipitously through the third quarter when they suddenly found strength and were positve in the single digits for the last quarter. Monthly declines in median price have been the order until the final quarter when median prices appear to have leveled out.

Looking from the annual perspective, home sales in December 2023 were up 3% over the last month of 2022. Using the same comparison, median prices were up 13%. This suggests the Harbor area may already be seeing improved stability.

Summarizing 2022 versus 2023 for the Harbor area, overall home sales volume dropped 17% for the year. Looking from a longer term perspective, sales have fallen 26% from the ‘pre-Covid benchmark year’ of 2019. From 2022 to 2023 the median price fell 2%. Again over the longer term, median prices in the Harbor area are up 31% over 2019.

Hill: Median Price Down – Sales Up

December home sales increased on the Hill by 9% over November levels. For the same mnthly period, median prices were down 9%. This pattern is expected to shift over the first quarter of 2024 as prices stabilize and interest rates decline to allow more potential purchasers to enter the market.

Compared to December of 2022, December 2023 came in with sales of 22% more homes and a median price increase of 5%. A solid year over year growth for the Hill.

Taking a step back and looking at the full year, sales volume fell 17% from 2022. At the same time, median price fell only 1%.

Inland: Sales and Prices Still Sliding

The last month of the year brought no relief for the Inland area. The number of homes sold continued to decline with sales down 2% compared to November. The median price was down for the second month, this time 5% for the month.

Looking at the same month last year, gives year over year sales volume down 2%,and a median price that’s down 2%. The final quarter of the year has been a rough adjustment period for the Inland area.

In the broader year over year view, the Inland area again fell, with sales volume down 11%. Median price was flat for the period with a tendency toward negative. It’s a transitional period which should resolve into a firmer picture by the spring of the year.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

Every city in California is required to present a general plan for housing development, which is to be updated each year. The general plan must take into account housing needs based on the population and expected population growth. However, what the general plan doesn’t account for is zoning laws, which currently take precedence over the general plan. This means cities can feign considerations in their general plan while implementing zoning laws that combat their own plan. Even cities that mean well may not be able to get sufficient votes to modify their zoning laws in accordance with the general plan.

That will change beginning January 1, 2024. Under AB 821, development plans that don’t meet zoning ordinances may still pass if the ordinance they fail to meet is inconsistent with the general plan. AB 821 allows for two possible outcomes in this scenario. The local agency controlling development applications has 180 days to either amend the zoning law that is inconsistent with the general plan, or simply process the development application regardless of failure to meet zoning laws. Note that this law doesn’t actually force changes in zoning ordinances. Nothing happens to zoning ordinances that aren’t challenged by a development application designed to further the general plan, and a very stubborn local agency could simply delay processing by up to 180 days, and then possibly a further 90 days in court.

The Tenant Protection Act (TPA) was originally passed in 2019, and outlines the conditions under which a landlord can legally evict a tenant. The TPA has been revised and updated in the past, and is receiving a new update with the passage of bill SB 567. The new law goes into effect April 2024, and adjusts the requirements for no-fault evictions, as well as setting the fine for a landlord’s violation of the laws at three times the cost to the tenant plus additional fines.

Under current regulations, a landlord can perform a no-fault just cause eviction if the landlord or their immediate family intends to occupy the residence, or the landlord intends to demolish or substantially renovate the residence. Under SB 567, mere intent isn’t enough. Rather than only planning to occupy the residence, the landlord or relative must have already occupied it for at least 12 continuous months as their primary residence. Demolition or renovation plans require a written notice including permits, a description of the plans, and an expected duration, as well as the opportunity for the tenant to re-rent the property at the same price if the plans don’t go through. There are other conditions under which a landlord can perform a no-fault just cause eviction, but they aren’t affected by SB 567.

The Regional Early Action Planning (REAP) 2.0 program was enacted in 2021 in order to achieve housing and climate goals, including infill development and appropriately priced housing. REAP 2.0 received its first round of funding in July of this year, and has decided where to allocate its grants. Over $352 million was awarded in grants.

Of this amount, $30 million was given to Higher Impact Transformative (HIT) communities. HIT communities are those that have demonstrated a commitment to underserved communities. For this round of funding, that includes the City of Oakland, the City of Rancho Cordova, Tahoe Regional Planning Agency (TRPA), San Diego Association of Governments (SANDAG), and Bay Area Rapid Transit (BART).

The majority of the funding went to Metropolitan Planning Organizations (MPOs), some of which also serve HIT communities. TRPA and SANDAG received funding in both categories. Most of the funding going to MPOs was awarded to the Southern California Association of Governments (SCAG) at $237.41 million. The other MPOs that received funding were Association of Monterey Bay Area Governments (AMBAG), Madera County Transportation Commission (MCTC), Sacramento Area Council of Governments (SACOG), and Shasta Regional Transportation Agency.

Representative Maxine Waters recently introduced the Downpayment Toward Equity Act of 2023, intended to help disadvantaged groups afford their first home. The bill would provide financial assistance for down payments, closing costs, and the costs to reduce interest rates for first-generation homebuyers who have not bought a home within the past three years. This mainly affects Black and Latine communities and could benefit up to around 5 million prospective homebuyers. However, while probably good-intentioned, this effort is not without its flaws.

We’re currently coming out of a historic peak in home prices. Prices have started to fall now, but they’re not going to suddenly bottom out overnight. It’s going to take a while for home values to fall. Pushing homeownership aid now is not the right time, for anyone, even if it’s directed at helping disadvantaged groups. And the last time minorities experienced a surge in homeownership turned out terrible for them in the end, albeit under different circumstances. In that case, it was predatory subprime lending that left minorities on the hook for massive mortgages with negative equity after the subsequent economic collapse. Of course, it’s doubtful that Waters’ intentions are predatory, but her plan could perhaps be better timed around the state of the economy.

In this November’s election, the Justice for Renters Act will reach the ballot. This bill would repeal the Costa-Hawkins Rental Housing Act, which is a 1995 state law that prohibits rent control for certain properties. Repealing it would allow local city governments more freedom in making decisions on rent control. This isn’t the first attempt — similar bills were put on the ballot in 2018 and 2020, but neither passed.

That doesn’t necessarily indicate a lack of support, though. What has actually happened in the past is that those who benefit from a lack of rent control are both more vocal and wealthier. Of course, it should come as no surprise that landlords are typically wealthier than those renting from them, and therefore able to contribute more campaign funds. But you may not be aware that renters are less likely to vote, particularly because non-citizens are more likely to rent than buy. In addition, the share of renters in California is slightly smaller than the share of homeowners. Even if homeowners also includes non-landlords, homeowners generally aren’t negatively impacted by high rent prices. This time, though, rent prices have become so exorbitant that the bill has a higher chance of passing this year.

Last week, the Federal Reserve, commonly known as the Fed, increased the federal funds rate by 0.25 points. The federal funds rate now sits at 5.25%-5.5%, the largest value in 22 years. In addition, the Fed made a statement regarding “determining the extent of additional policy firming that will be appropriate.” Policy firming refers to rate increases.

Barclays, a multinational bank based out of the UK, also noted a change in the Fed’s language regarding this policy. A prior statement by the Fed referenced “the extent to which additional policy firming may be appropriate.” Their new statement is significantly more certain about the appropriateness of additional policy firming, leading Barclays to believe that the Fed plans additional rate increases. Barclays predicts this will probably happen in September or November, which are the next two times the Fed meets.

However, it’s important to realize that the federal funds rate is not the same as mortgage interest rates. In fact, they aren’t directly related at all. Mortgage interest rates do frequently increase when the federal funds rate increases, but there are additional factors at play. These include demand and economic outlook. Both of these are somewhat mixed. Demand is not particularly high, but neither is supply. Our economy is currently in a recovery cycle, so it’s looking up, but isn’t necessarily stable. So, it’s definitely a possibility that interest rates increase some more, but not a guarantee.

Starting from the beginning of 2023, and going until 2032, the federal government has announced tax credits for improving the energy efficiency of one’s home. Some of the credits apply only to primary residences; others apply to both primary residences and second homes. In either case, a tax credit of 30% of the cost of improvements can be applied to federal income tax.

The energy improvements that apply to either type of residence are rooftop solar panels, wind energy improvements, geothermal heat bumps, and battery storage. The types of improvements that apply only to primary residences, as long as they are energy efficient varieties, are heat pumps, heat pump water heaters, insulation, doors, windows, and electrical panel upgrades. This tax credit also applies to home energy audits. The primary residence only tax credit has a limit of $3200 annually.

If you’ve ever bought a home, chances are you’ve heard of a property being “in escrow.” But what does this actually mean? Escrow is the term for a neutral third party holding funds and documents to be disbursed during a real estate transaction. This is typically either an escrow officer or a title company, and even if it’s a company, the entity will be referred to as the escrow officer. The reason for this is to safeguard funds to avoid misallocation or fraud, which is why it’s important that the escrow officer is trusted by all parties involved.

The escrow process is initiated when the buyer and seller open an escrow account and deposit the funds after agreeing on the terms of the transaction. This is also when the buyer deposits their earnest money and the escrow officer collects all necessary documents, such as the purchase agreement, title documents, and loan documents, among others. Once escrow is initiated, the buyer will then have a period to investigate the property and conduct inspections. If the buyer finds any issues during this period, that’s when they can request repairs or renegotiate the agreement. Once the buyer is satisfied, the next step is to remove contingencies, after which the transaction enters the closing process. During the closing process, the escrow officer prepares closing documents and coordinates signatures. Only after the documents are signed by all parties can the funds be disbursed and title transferred to the buyer.

It’s common nowadays, though not necessary, to use living trusts to hold real property. It’s also a common misconception that the trust owns the property. Trusts are complex, and contrary to what one may think, don’t actually get any simpler when there’s only one trustee. A trust is always an agreement between a trustor and a trustee. This doesn’t change even if they’re the same person, which is definitely possible, but you still need to know the difference.

The trustor is the person who creates and funds a trust, and sets the terms, beneficiaries, and trustees. The trustor is usually only one person, but could be a married couple. The trustor could also be a trustee, and often is when the trust is created, but may not be. Trustees, on the other hand, manage the trust and perform day-to-day tasks in accordance with the directions given in the trust. There could be any number of trustees. These are the actual owners of real property, not the trust itself. If at any point all trustees are deceased or unwilling to act, the trustor can appoint a new trustee, or the court can do so if the trustor is not able to or not allowed to by the trust’s provisions.

Trustees are also responsible for signing the certificate of trust that would be provided to the title insurance company. This document must have the date of the trust’s creation, identity of all trustors and trustees and whoever can revoke the trust, powers of the trustees, manner in which trust assets are taken, legal description of the property or whatever part is held by the trust, signatures of trustees, and a statement that the trust certification is still valid and correct. Normally, all trustees must sign, but there could be provisions in a trust that allow for less than all of them to sign. Trustees may give someone power of attorney only if the trust specifically allows for it.

California has a long list of protected classes under its fair housing laws. Landlords are forbidden from refusing tenants on the basis of being in a protected class. People with a criminal history, however, are not a protected class, and landlords are allowed to request a background check and base their decisions on it. So landlords may not be aware that it is illegal have a blanket ban on tenants with criminal history. Why is this the case, then? The answer is implicit discrimination.

It’s well known that racial minorities, particularly Blacks, are heavily disproportionately criminal record holders. Regardless of the reason for this fact, it’s true that blanket bans on criminal record holders do therefore disproportionately affect racial minorities. Because of this, California law prohibits these blanket bans. It is, of course, also illegal for landlords to only conduct background checks on members of specific protected classes, but this shouldn’t come as a surprise. In addition, landlords cannot reject tenants on the basis of suspected criminal activity without a criminal record, nor on the basis of gang affiliation. Despite the association of gang affiliation with probable criminal activity, it is not actually illegal to simply be a member of one.

Some parents want to help their kids any way they can, including by helping them pay their mortgage. Or perhaps they’ve suggested that their inheritance be used for this purpose. Others want to instill the importance of financial responsibility or independence. Some simply can’t afford to help. But if you do want to help your kids with their mortgage, there is some important tax information you should be aware of.

One very common way for parents to assist their kids is with a financial gift. This isn’t just as simple as giving them money. Financial gifts above a certain amount per year do need to be recorded, and may be subject to a gift tax. In 2023, this amount is anything over $17,000 annually, but this value could change each year. Income tax could come into play if instead of gifting your child money, you provide them with a loan. The interest you receive on the loan must be reported as income and may be subject to income tax, and may also be deductible for your child. Capital gains tax is relevant if your kid inherits a property from you or you gift them a property. In the case of a gift, when your kid sells the home, they will need to pay capital gains tax if the home appreciated in value. In the case of inheritance, the capital gains tax amount is based only on the amount of appreciation and not the total value of the home.

At the start of May, the Federal Housing Finance Agency (FHFA) modified the fee structure for loans guaranteed by Fannie Mae or Freddie Mac. The goal of the change was to increase the accessibility of homeownership to disadvantaged groups. In order to achieve this, fees were reduced for low-income borrowers, first-time homebuyers, and those with credit scores below 680.

However, reducing some fees meant needing to increase fees elsewhere. Fees increased significantly for middle income earners, those making larger down payments, cash-out refinance applicants, and second-home buyers. Critics argue this is a bad idea, since middle-income earners are more ready to buy and less risky to lend to. But despite the fee increases for middle-income earners, fees are still lower the higher your credit score — that hasn’t changed. If the changes push middle-income earners away, the effect is probably psychological, not necessarily financial.

Two measures went into effect this spring, Measure GS in Santa Monica on March 1st and Measure ULA in Los Angeles on April 1st, both of which enact an additional transfer tax on the sale of very expensive homes, dubbed the Mansion Tax. Measure GS affects properties sold at over $8 million and Measure ULA has two tiers, one affecting properties sold at over $5 million and another affecting properties sold at over $10 million.

Prior to these measures, the transfer tax in both cities was a small dollar value per $1000 of purchase price regardless of property value. Including county taxes, this value is $5.60 in Los Angeles, and Santa Monica has two tiers, one at $4.10 per $1000 and another at $7.10 per $1000. Measure GS added a third tier to the Santa Monica system, which is a significantly higher $56 per $1000 value for homes over $8 million. Los Angeles still only has one base value of $5.60 per $1000, but with an additional tax of 4% for homes between $5 million and $10 million, and 5.5% for homes over $10 million.

The business lobby in California, and in particular the California Chamber of Commerce, has had quite a lot of success taking down bills that they deem “job killers.” Many of these bills are not at all designed to kill jobs, but rather to improve conditions for employees. To the business lobby, these are the same thing, but these are often the types of bills that the majority of the populace in California would tend to support.

One of the bills the California Chamber of Commerce is targeting is a bill to tax total wealth on individuals with a net worth of $50 million or more. Introduced by Milpitas Democratic Assemblymember Alex Lee, the bill would be the first of its kind if it passes. Obviously, there have been taxes on income, but so far, none on net worth. Lee’s argument is that the stocks and properties owned by the ultra-wealthy allow them to legally borrow and transfer funds in a way that avoids a significant percentage of income taxes. According to the chamber, this would simply convince the ultra-wealthy to leave California, rather than increase tax revenues.

The second bill was proposed by Los Angeles Democratic Senator María Elena Durazo. The bill would increase the minimum wage for health care workers to $25 per hour. According to Durazo, health care workers — especially whose who are women or people of color — frequently take home poverty wages, despite working multiple shifts due to being understaffed. The chamber argues that increased payroll costs for health care facilities would simply be passed onto patients, reducing health care affordability.

The chamber has a similar argument against the proposal to increase the required minimum paid sick days offered per year from three to seven, claiming that either the costs will be passed to consumers or the employers will cut benefits or lay off workers. Long Beach Democratic Senator Lena Gonzalez, who introduced the bill, says that the current sick leave is not adequate and forces employees to either forego pay to stay home or risk infecting coworkers.

SB 9, also called the HOME Act of 2021, is a California law requiring cities to allow homeowners to subdivide lots into potentially up to 4 units. This law makes it significantly easier to built accessory dwelling units (ADUs). Huntington Beach has decided it doesn’t like this, and is willfully ignoring the law, stating that they won’t process ADU applications. The City Council has even gone as far as to enact an ordinance declaring that they are exempt from some of the requirements of the Housing Accountability Act (HAA). The HAA streamlines the approval process for low- and moderate-income housing. Huntington Beach is not compliant with HAA requirements, and so the city is attempting to declare that the regulations simply don’t apply to them.

This is entirely illegal on the part of Huntington Beach, and so naturally, it hasn’t gone over well. The city has received letters from the Department of Housing and Community Development (HCD) and has been sued by the California Office of the Attorney General (OAG). Knowing that the state does have authority in this regard, the Huntington Beach City Council is starting to backpedal. But this probably isn’t the end, nor was it the beginning. Huntington Beach has already been sued previously by the state for housing law violations, settling in 2020 and losing millions of dollars in state funding.

Until the end of January 2023, the City of Los Angeles has been under its own eviction moratorium laws, separate from those of the county as a whole. The city’s moratorium has ended. However, the county’s moratorium isn’t over yet. Every city in LA County is now under the county’s moratorium rules.

With the LA City rules gone, tenants are no longer able to defer rent payments. But note that the rent freeze is separate and not part of the eviction moratorium. Rents still cannot be raised on rent-controlled properties in Los Angeles until January 31, 2024. Under the county eviction moratorium, evictions are allowed only under certain circumstances. If the circumstances are related to COVID, it’s very likely that the landlord cannot legally evict. Also, use of the Ellis Act to evict tenants by removing the property from the rental market is still not permissible until April 1, 2023. If the tenant breached the rental contract, though, the landlord is probably able to evict, with a few exceptions.

A little known fact is that lease agreements actually establish two entirely separate legal relationships between the landlord and tenant. The first is a right of possession granted to the tenant, and the second is a list of contract rights, which is what allows the landlord to collect rent. Though the lease agreement establishes both of these, they can be cancelled separately and through different means, though certain actions can cause both to be cancelled simultaneously. Cancellation of the right of possession is termed a forfeiture, and cancellation of the contract rights is called a surrender.

Because a tenant can’t unilaterally forfeit their right to possession or have the landlord surrender their contract rights, it falls on landlords to follow the proper procedures when a tenant chooses to vacate the property or stop payments. A savvy tenant could escape paying missed rents if the landlord unwittingly cancels the contract rights. On the other hand, a savvy landlord could put a former tenant on the hook for missed rent payments if they follow all the legal procedures, though one of the legal procedures involves notifying the former tenant, so this isn’t necessarily easy.

It’s always in a vacating tenant’s best interest for the contract rights to be surrendered. Landlords need to be careful of following the law when attempting to lease a property that is legally still in a vacating tenant’s possession, but it’s not always in their best interest to initiate a forfeiture. The landlord could instead act as the tenant’s agent in subletting the property, while continuing to collect rent from the tenant for the remaining duration of the lease agreement. However, to do this, the term of the sublease must end on the same date as the existing lease agreement, otherwise the landlord is considered to have illegally given possession to a new tenant while the former tenant still retained it.

In recent years, a few states have created laws regarding pay transparency in an effort to reduce discriminatory wage gaps. Colorado was the first to introduce a statewide law in 2019, though it didn’t take effect until 2021. New York City’s law will soon expand to all of New York. A new law just took effect in Washington as well as our own state, California, on January 1st. California’s law requires that companies with at least 15 employees post pay ranges in their job listings, as well as requiring that current employees have access to the pay range for their current position. The penalty for violating this requirement is between $100 and $10,000 per violation. The first violation only gets a warning as long as the information is added. Some companies also don’t currently have pay bands — the new law requires them. Companies with at least 100 employees will need to provide more detailed information.

Unfortunately, the new law may have to contend with some resistance. In New York City, employers chose to display incredibly wide price ranges. This doesn’t help prospective employees at all to figure out how much they would actually be getting. In one extreme example, Citigroup claimed a range of $0-$2 million, though they later said this was a computer glitch and changed it to something more reasonable. In Colorado, employers created remote job openings — with the stipulation that they could not be in Colorado, so the state requirement didn’t apply to that listing. Colorado’s method probably wouldn’t work in California, since California has such a large population that employers would miss out on a huge segment of potential employees. But New York City’s method is actually already in use in California, even without a requirement to list pay ranges at all. This is because prospective employees tend to disregard a listing entirely if there’s no pay range provided.